The Energy Infrastructure Newsletter • Spring 2021

As an investment advisor, you have been subscribed to the Energy Infrastructure Newsletter so that you and your clients can stay abreast of this powerful emerging subsector. Formerly the MLP Newsletter, the Energy Infrastructure Newsletter is published in partnership with the Energy Infrastructure Council, a nonprofit trade association dedicated to advancing the interests of companies that develop and operate energy infrastructure. EIC addresses core public policy issues critical to investment in America’s energy infrastructure.

Future of Midstream Hitched to Consolidation and a Pivot Toward Renewables

Today’s EIC Newsletter features an interview with Spiro Dounis, the lead research analyst covering MLPs and midstream equities for Credit Suisse, a global investment bank, wealth advisor, and financial services firm. Mr. Dounis has more than 10 years of experience in the energy industry, covering coal, shipping, refining, and midstream

Advisor Access: What are midstream investors focused on as we move beyond 2020 and closer to recovery from an economy slowed by the COVID-19 pandemic?

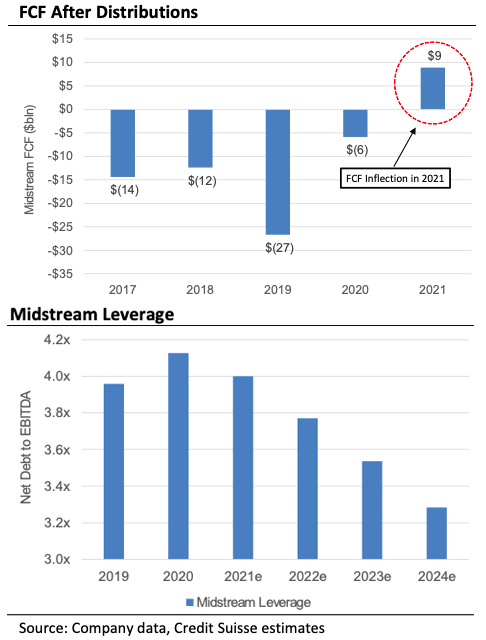

Spiro Dounis: Much like the rest of investors in energy, midstream investors are still very focused on capital returns and lower leverage. Midstream companies are now utilizing share repurchases as a capital return tool—a slight departure from the high dividend payout model of the past. For many, though, leverage is the primary focus, and likely a multiyear process for this sector. These initiatives were already underway before the pandemic, but the events last year seem to have hastened the process toward more capital discipline and lower leverage.

That’s not to say investors still can’t benefit from yield. The companies we cover yield between 8–9%, compelling by most standards in this low-rate environment. From a free cash flow (FCF) perspective, we calculate FCF yield of 13–14%. While some of that excess yield may come in the form of share repurchases, we expect the vast majority to be used for deleveraging—and that’s not necessarily a bad thing for equity holders. Back in 2019, almost none of our coverage could support the dividend with free cash flow; in 2021 we expect 90% of our coverage to be able to support the dividend with FCF.

AA: Is it too early to talk about dividend growth or earnings growth for this sector?

SD: It’s not too early, but it is early. Midstream companies are under pressure on two fronts: lower tariffs and lower volumes. The sector largely over-built pipeline capacity, and that usually means lower tariffs when those contracts come up for renewal. On volumes, most basins are declining year over year. Even some premium basins, like the Permian, are targeting flat.

Producers are firmly committed to capital discipline, and that means fewer opportunities for midstream companies to expand. That said, commodity prices have rallied and put most basins back into solid economic territory, setting up the potential for growth again in 2022.

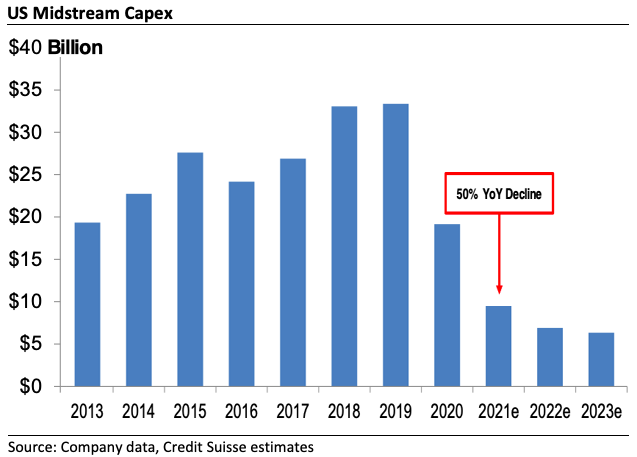

We’re sanguine about the potential for growth again, but don’t see many opportunities for robust capital programs in the near or medium term. We expect midstream capital spending to decline by roughly 50% in 2021 versus 2020—that likely means no or slow growth for now.

AA: If growth isn’t the allure of the midstream sector currently, what is?

SD: We believe the sector offers interesting asymmetry and optionality at this point. On the former, we just witnessed how durable these businesses can be—they’ve been battle-tested during the pandemic. While many had to cut dividends and make difficult decisions, we found it very encouraging that several companies were able to meet and/or exceed their pre-pandemic earnings guidance. We didn’t see widespread bankruptcies or asset fire sales. In a way, these companies are emerging from the pandemic with stronger balance sheets, leaner cost structures, and more capital discipline. From an upside-downside perspective, we just witnessed the downside and these companies proved fairly durable.

On optionality, we don’t believe the sector is pricing in growth. To the extent we enter into another growth cycle, the sector has upside to both earnings and valuation. In other words, we don’t believe investors are paying for growth at current valuation levels.

AA: What risks do investors need to be aware of?

SD: In the short term, risks include weakening commodity prices and slower growth. Commodity prices currently support modest growth in 2022, but that dynamic is tenuous if global supply (i.e., OPEC production) increases meaningfully. Beyond supply, any event that short-circuits recovery of demand could also be problematic. Several management teams have pointed to new virus variants as reasons for their conservative guidance.

Longer term, it’s hard to talk about risks for this sector and not mention energy transition. We don’t see the demand for hydrocarbons going away anytime soon. In fact, most global studies and climate scenarios have hydrocarbons remaining a large part of the energy mix through 2050. For us, it’s more about the direction of travel, with use of hydrocarbons in a slow decline. When you are a public company, attracting new capital to your stock becomes very challenging when the demand for your product is declining each year into perpetuity. That can have meaningful impacts on valuations and terminal values. Our analysis showed terminal values were cut in half from 2019 to 2020. Some ground has been regained, but the market still appears reticent to ascribe long-term value to these stocks.

AA: Are there opportunities for midstream in the energy transition, or is it all a threat?

SD: Call us optimists, but we see opportunities for this sector. Even a green economy is going to need logistics and infrastructure. This sector has decades of experience and vast infrastructure in place that can be repurposed. The question is: Can these companies evolve quickly enough to ensure they have a place in the energy transition?

Several management teams have begun laying out initiatives on this front. We’re hearing more about renewable diesel (refined from plant or animal fats) and renewable natural gas (gathered from waste products found at dairy farms and landfills), hydrogen, carbon capture, and solar. Many refined products pipelines and terminals can be repurposed to accommodate renewable diesel. Renewable natural gas has the same physical properties as conventional natural gas. Hydrogen can be blended into the current natural gas network or moved on a dedicated pipeline with some retrofitting. Carbon capture is going to be a critical component to achieve 2050 net zero goals—several companies are exploring opportunities there, too.

AA: What about regulatory risk?

SD: That’s not new to this sector. Even during the Trump Administration, when federal policy was more favorable to conventional oil and gas production, pipelines faced considerable pushback at state and local levels. Courts have been an effective tool in preventing, or at least slowing, pipeline progress. That said, the challenges presented by the new Biden Administration come at a time when the midstream sector is still trying to recover.

At this point, we don’t expect any large-scale pipelines to be built in the near or medium term. The regulatory risks are too high and, in some cases, the market just doesn’t need them. The recent moratorium on federal leases shouldn’t have a material near-term impact on this sector, but does limit longer-term growth. The current administration sent a clear signal in the first few weeks of its tenure when it revoked the Keystone Pipeline’s permit and halted new federal oil and gas leases.

AA: With a shrinking total addressable market and higher regulatory risk, what is the next step for the midstream sector?

SD: We believe the sector needs to consolidate. In fact, the process is already underway—just a few years ago the sector had over 100 public midstream companies. That figure has been cut in half.

We also look to other energy sectors in more mature stages of their life cycles, like refiners, for guidance on midstream’s future. The refining sector has consolidated over the last two decades, and embraced the low-leverage, capital-discipline, high-capital return model before it was cool. We believe midstream is gravitating in that direction to consolidate bargaining power and prevent oversupply. From a stock market perspective, consolidation should also result in larger, well-capitalized, investible companies.

That said, consolidation progress has been slower than some would like. Management teams all seem to agree that consolidation is needed, but balance sheets are preventing progress. In our view, consolidation becomes more realistic after 2021, when earnings have stabilized and balance sheets are right-sized.

AA: Thank you, Spiro.

Spiro Dounis joined Credit Suisse as a Director in 2018 to lead coverage of the midstream space. Mr. Dounis has covered the energy sector in various capacities for more than 10 years and was recently ranked by Institutional Investor. Prior to joining Credit Suisse, Mr. Dounis led coverage of the refining and shipping sectors at UBS. He was also a member of the MLP team at JP Morgan, where he led upstream MLP coverage. Mr. Dounis is a Certified Public Accountant and a CFA Charterholder. He resides in Garden City, N.Y., with his wife, Michelle, and two children.