The REIT Newsletter for Advisors • Summer 2023

Industrial REITs Remain a Darling Real Estate Sector

by Ed Pierzak, PhD, Senior Vice President, Research, Nareit

Industrial REITs own and manage industrial facilities and rent space in those properties to tenants. Typical tenants may include firms like Amazon, Home Depot, Wal-Mart, FedEx, UPS, and DHL. Some industrial REITs focus on specific types of properties, such as warehouses and distribution centers. Industrial REITs play an important part in e-commerce and are helping to meet the demand for rapid delivery. Some have a global footprint.

Industrial REITs have enjoyed strong stock market performance over the past three years reflecting the increased demand for space driven by e-commerce logistics needs. Since February 2020, industrial REITs are the second-best performing REIT sector and outperformed the broader stock market (Russell 1000). During 2023, the industrial sector is also the second-best performing REIT sector, up nearly 9% though mid-June.

The U.S. economy has been facing numerous headwinds including elevated inflation, rising interest rates, and a banking crisis. At the end of the first quarter of 2023, the Bloomberg consensus forecast survey placed the odds of a U.S. recession within the next 12 months at 65%. The commercial real estate mortgage market has also changed dramatically since the end of 2021. For many real estate investors, gone are the days of low-cost, readily available property financing. Today, borrowers face significantly higher interest rates and stricter underwriting standards. Despite these headwinds, industrial REITs continue to be well prepared to navigate this period of economic and capital market uncertainty.

With demand outstripping supply, industrial has remained a darling sector for real estate investors. According to CoStar data as of the first quarter of 2023 (the latest data available), industrial enjoyed a near all-time high occupancy rate of 95.7% and annual double-digit rent growth of 10.3%. From a property fundamentals perspective, industrial is the best positioned sector of the four traditional property types.

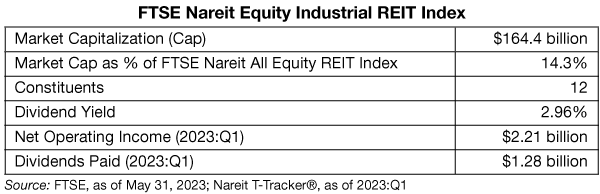

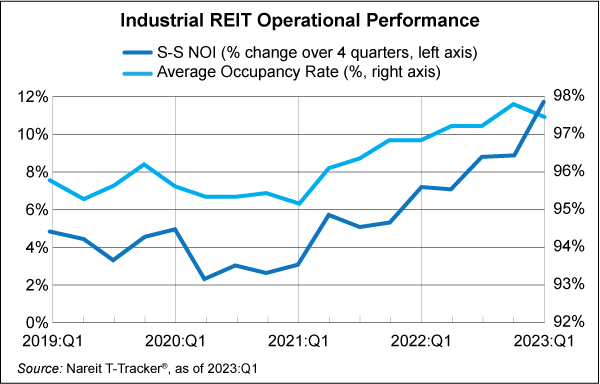

Data from the Nareit Total REIT Industry Tracker Series (T-Tracker®) for the first quarter of 2023 (the latest data available) show that industrial REITs have delivered exceptional operational performance. From an operations perspective, on average, industrial T-Tracker® data show that:

- Same-store net operating income experienced an 11.6% year-over-year gain, underscoring that industrial REITs are keeping up with inflation.

- Average occupancy remained at lofty levels; it stood at 97.4%, approximately 60 basis points higher than one year ago.

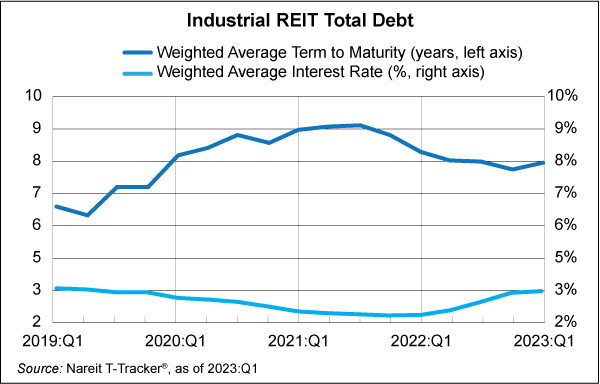

While industrial REITs have not been immune from the current mortgage market turmoil, T-Tracker data show that they have been reasonably well-insulated from it. On average, industrial REITs have maintained long-term, well-structured balance sheets with low leverage ratios, predominantly utilizing unsecured debt and fixed interest rates. Specifically, industrial T-Tracker® data show that:

- Leverage ratios remained near historical lows with debt-to-market assets at 22.0%.

- Unsecured debt accounted for 84.6% of total debt.

- Fixed rate debt accounted for 87.0% of total debt.

- Weighted average term to maturity of industrial REIT debt was 97.0 months, or slightly more than 8 years.

- Weighted average interest rate on total debt was 3.2%.

The recent divergence of U.S. public and private real estate markets in 2022 has increased industrial REITs’ attractiveness. Differences in capitalization (cap) rates capture the U.S. public-private real estate market divergence. A cap rate is often used as a real estate valuation metric. It measures the ratio of a property’s net operating income to its value. Typically, a higher cap rate translates to a lower price.

As of the first quarter of 2023, T-Tracker data show that the industrial REIT implied cap rate was 4.1%, which was approximately 90 basis points higher than the industrial private market appraisal cap rate. All else being equal, this cap rate spread suggests that industrial REITs are priced more than 20% below their private counterparts.

A review of historical market dynamics also shows that industrial REIT total returns have tended to bounce back—and even surge—after periods of significant REIT underperformance relative to private industrial real estate (relative performance troughs). Post-trough analysis from 2000 to 2022 shows that industrial REIT four-quarter total returns averaged 55.5%; the private industrial real estate average was 6.6%.

Economic headwinds, mortgage market turmoil, and the divergence of U.S. public and private real estate markets have created an interesting property investment environment. Industrial REITs continue to be well-prepared to navigate this period of uncertainty. The current cap rate spread has increased the attractiveness of industrial REITs. Today, they offer investors access to institutional quality properties with best-in-class operators at substantially discounted prices relative to the private market. Industrial REIT total returns have also tended to bounce back—and even surge—after significant public and private real estate market dislocations. With these factors in mind, investors should stay attuned to the potential opportunities that industrial REITs may offer amid the uncertainty.

In closing, industrial REITs represent one of 12 property sectors in the U.S. REIT industry. They, along with their REIT counterparts, offer investors access to a wide range of real estate sectors while historically providing a steady stream of high dividends, the potential for long-term capital growth, and diversification which is why 83% of financial advisors recommend REITs to their clients. REITs are particularly critical in today’s economic environment because they have historically offered protection against inflation and recent research shows that REITs’ strong balance sheets have helped them remain resilient to higher interest rates.

Key numbers to remember:

11.6%

Beating inflation, industrial REIT same-store net operating income grew by 11.6% year-over-year in the first quarter of 2023.

20%

All else being equal, the industrial cap rate spread suggests that industrial REITs are priced more than 20% below their private market counterparts.

55.5%

On average, industrial REITs outperformed private industrial real estate, 55.5% to 6.6%, in the four-quarters after a relative performance trough from 2000 to 2022.