The REIT Newsletter for Advisors • Fall 2021

Do Homeowners Need REIT Investments?

By Nicole Funari, Nareit Vice President, Research

Investing in commercial real estate through REITs can help improve portfolio performance in a number of ways. REITs help diversify portfolio exposures, reducing overall risks, while also generating a high level of income and a competitive total return.

Investing in commercial real estate through REITs can help improve portfolio performance in a number of ways. REITs help diversify portfolio exposures, reducing overall risks, while also generating a high level of income and a competitive total return.

Investors who are homeowners may ask what the additional benefits to investing in REITs are, given their housing provides them with some exposure to real estate markets. The short answer: Homeowners can benefit because investment in income-producing commercial real estate is very different than investment in owner-occupied residential real estate. For example, long-term returns in REITs have outpaced homeownership returns over time, even accounting for the imputed value of rent.

Owning a home is primarily about having a place to live, although it often produces capital gains over time. Homeownership does not, however, typically generate current income, but rather requires regular mortgage interest payments, real estate tax payments, insurance payments and maintenance costs. Moreover, the long-term investment returns of homeownership generally lag behind REITs, even taking into consideration the value of the home as shelter.

Investment in commercial real estate, which is accessible to everyday investors through REITs, provides valuable diversification benefits for long-term investors, while also providing competitive returns. An estimated 44% of U.S. households are invested in REITs, mostly through retirement accounts. Among the benefits: REITs generate continuing income flow from rents and are a liquid investment diversified across a range of real estate properties in a variety of geographic locations. Investors can choose the amount to invest in REITs without having to buy an entire property. REITs also face different economic drivers than residential housing, and REIT returns have a low correlation with both the broader stock market and homeownership returns. Measuring returns over four years, the correlation between REITs and homeownership is 0.46.

By comparison, a house is comparatively illiquid; investment risk is not diversified but highly concentrated and, as mentioned above, owning a home also does not typically provide income to owners who live in that home.

Fortunately, real estate investment does not have to be an either/or scenario — both homeownership and real estate investment through REITs have specific long-term benefits and possibilities.

Comparing returns since 2000, REITs have proven to be a valuable investment. Chart 1 shows the quarterly price and total returns over time. REIT returns include dividends and homeownership returns include imputed rent — the rent owners are implicitly paying themselves by living in their homes. Even including imputed rental value, REITs provide stronger long-term returns. For $100 invested in REITs starting in 2000, the investor would have $902 at the end of the first quarter in 2021, an 11% compound annual growth rate. A homeowner’s $100 investment would be worth $553, an 8.5% compound annual growth rate.

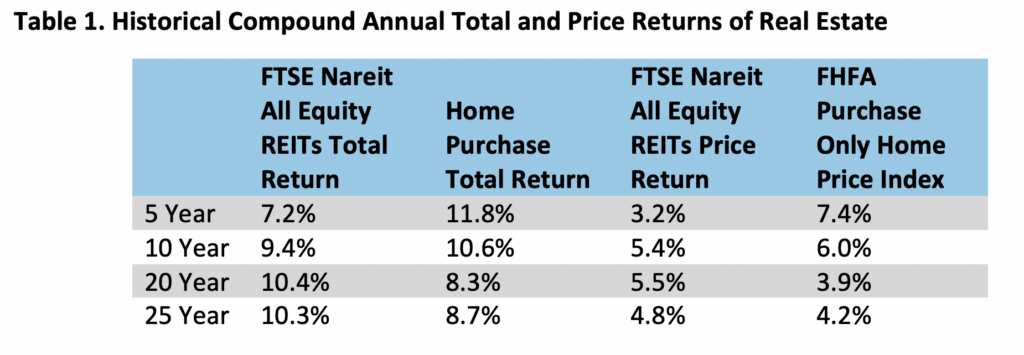

Table 1 compares the compound annual price and total returns for REITs and single family homeownership over various holding periods. Across time periods, we can see that over the five- and 10-year windows, homeownership has outperformed REITs, driven by price returns. However, most homeowners keep their homes longer than 10 years. According to the American Community Survey, 50% of homeowners stay in their homes 13 or more years, and over an investor’s lifetime, homeowners are likely to have multiple decades of ownership in a number of individual homes. For durations over 10 years, REITs outperform by a healthy margin.

Source: Nareit analysis of FTSE-Nareit All Equity Index (total and price returns) and FHFA Purchase Only Home Price Index as of Q1/2021. Total homeownership returns derived from Davis, Morris A., Lehnert, Andreas, and Robert F. Martin, 2008; data located at Land and Property Values in the U.S., Lincoln Institute of Land Policy. Total return reflects price appreciation and rental value, property taxes and capital expenditures are not included.

The homeownership returns shown above are based on national averages. But for single family homeowners, their houses are in one market in one geographical location, resulting in less diversification and more volatility in returns than implied by the national index.

REIT investors can invest in funds that mirror the broad index — representing over 500,000 structures — or buy individual REIT stocks. Even individual REIT stocks provide returns for a portfolio of structures. Chart 2 shows how volatility increases when home prices are indexed in more narrowly defined geographical areas. As the volatility in price returns increases from left to right, this reduces the risk-adjusted return as shown by the Sharpe Ratio.

To summarize: While there continue to be benefits to individuals who pursue homeownership, REIT investment is a good way to complement investment in a home.