The REIT Newsletter for Advisors • Spring 2021

Past as Prologue:

2020 and REIT Performance in 2021

by Calvin Schnure

Nareit Senior Vice President, Research & Economic Analysis

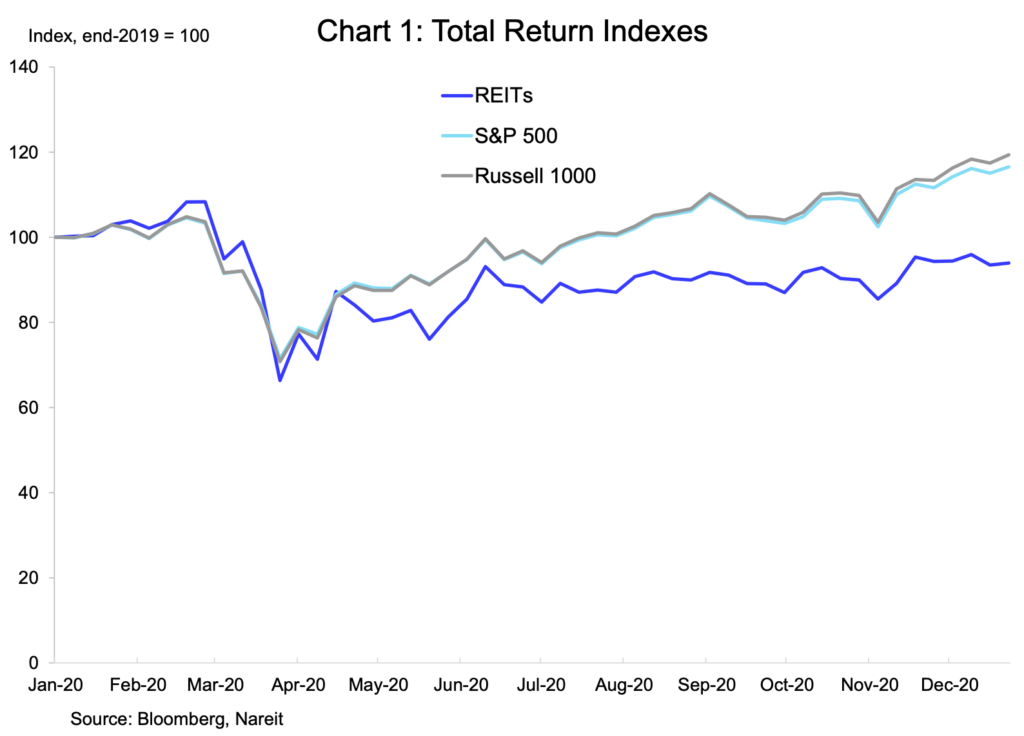

The year 2020 is officially in the history books. Despite fervent desires to block out memories of last year, a brief retrospective of REIT stock market performance during the pandemic can provide insights into what to expect in the year ahead.

As this report demonstrates, the historic stock market declines during the periods of greatest uncertainty in the pandemic were partly or completely reversed when market reality proved less threatening than initially feared. Real estate markets have been the focus of some of these concerns, especially that the pandemic may have caused long-term shifts in how real estate is used—think “work from home” and “Amazon deliveries”—and that these shifts may continue to influence REIT performance well into the future.

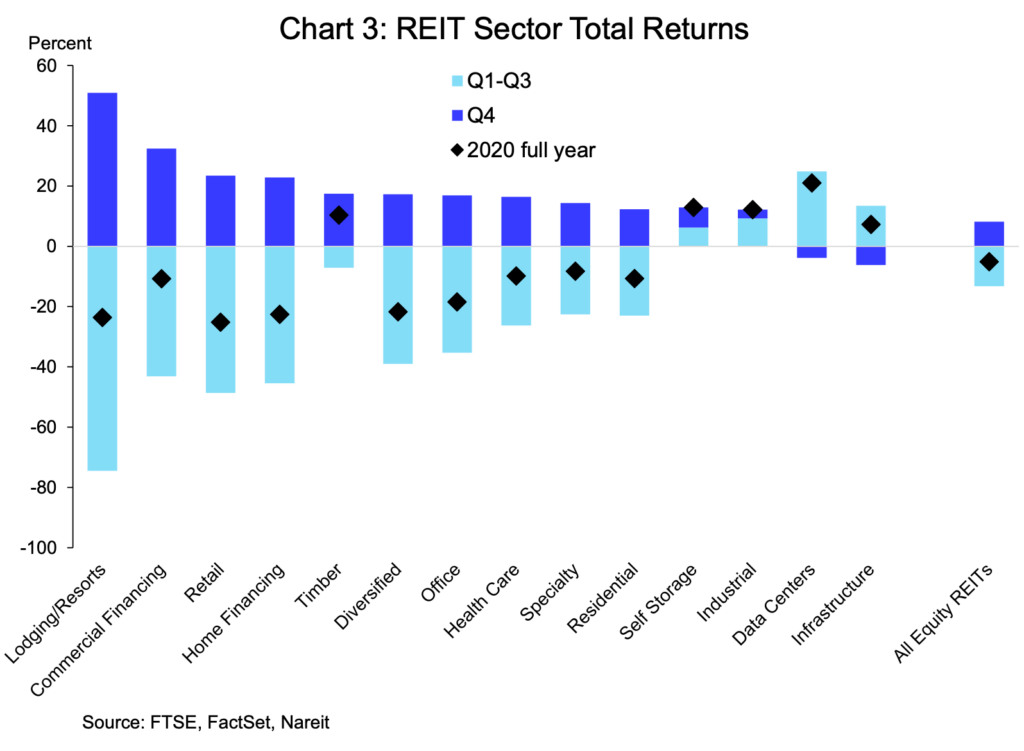

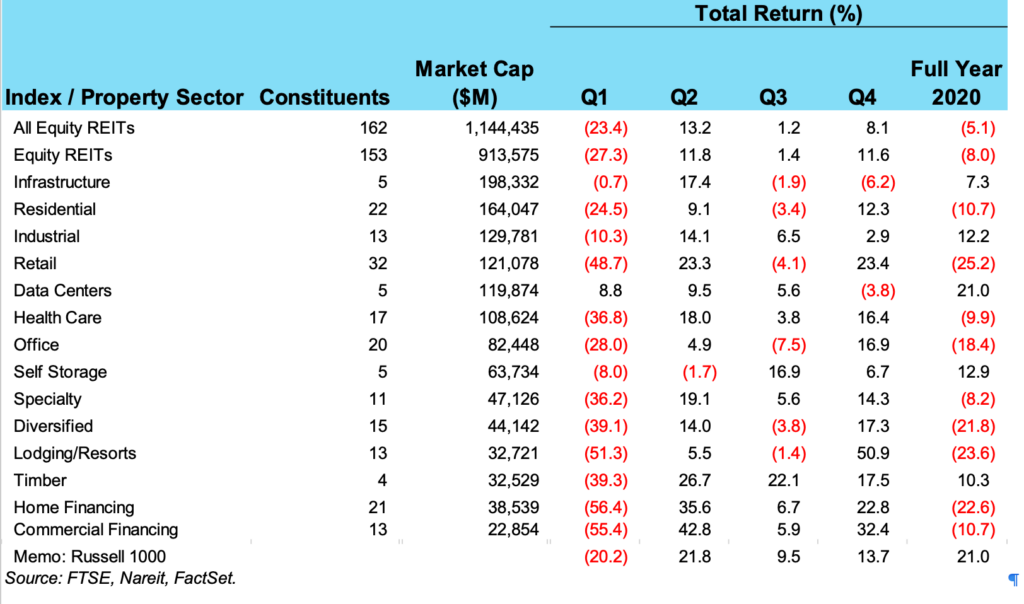

REITs lagged the broader market during much of the mid-year recovery after the initial plunge, perhaps reflecting these longer-term concerns. Markets have rallied since initial vaccine results were released, however, and the REIT sectors that suffered the largest declines last spring have posted impressive gains—for example, lodging/resorts had a total return of greater than 50% in the fourth quarter of 2020. This rally has continued in early 2021, with retail REITs recording a total return of 18% year to date as of mid-February, and the regional mall REIT subsector posting a return of 34%. Should these trends continue in the months ahead, REITs may outperform the broader market in 2021.

The Pandemic Produced Some Winners

Several REIT sectors support the digital economy, and these experienced a surge in demand during the pandemic. These include infrastructure REITs, which own cell towers that transmit both voice and data communications; data center REITs, which house the servers that process and store those communications and host web pages on the Internet; and industrial REITs, which own logistics facilities to help transport goods purchased through e-commerce.

REITs in these tech-linked sectors performed critical functions for American businesses, consumers, and households as they adapted to life during the pandemic. The strong demand also boosted current earnings and expected future earnings growth, resulting in robust stock market gains in the first half of the year.

The Vaccine Rally Closed Out 2020

The announcement of successful vaccine trials, and the subsequent emergency use authorizations enabling distribution of two vaccines against COVID-19 (with a third approval expected Feb. 26), have brought hope that the pandemic can be contained in the months ahead. The prospect that the end may be in sight spurred broad increases in REIT share prices.

The vaccine rally was especially pronounced among the REIT sectors that declined most in early 2020, as demonstrated by the fourth quarter performance of lodging/resort REITs. Other sectors with gains greater than 20% included retail (23.4%), home financing (22.8%), and commercial financing mREITs (32.4%). Nevertheless, these impressive gains still left these sectors in negative territory for the year as a whole.

News of the vaccines, however, had a negative impact on the tech-related property sectors that had outperformed earlier in the year. Total return for infrastructure REITs was 6.2% in the fourth quarter, and –3.8% for data center REITs. These declines merely trimmed the gains from earlier in the year, however, with both these sectors, as well as self storage, industrial, and timber REITs, in positive territory for the year as a whole.

Early Reports on Q4 Earnings Confirm Recovery Is Underway

REITs have begun reporting fourth-quarter earnings. While earnings season remains incomplete, several themes are apparent from the news to date.

First, the sectors that bore a strong negative or positive impact from the early phases of the pandemic continued to feel its effects in the fourth quarter:

Second, on the downside, funds from operations (FFO, a commonly used measure of earning performance for REITs) of lodging/resorts and retail REITs remain well below pre-pandemic levels. As shoppers venture back into the stores and malls, these earnings figures are likely to improve, but a more complete recovery is unlikely until the pandemic is vanquished.

Third, on the upside, the tech-linked sectors that support the digital economy—data centers, infrastructure, and industrial REITs—enjoyed robust earnings growth in the fourth quarter compared to one year ago.

The other property sectors, which represented about half of pre-pandemic FFO, have shown signs of returning to normal, and are on track to recover half or more of the initial decline in earnings.

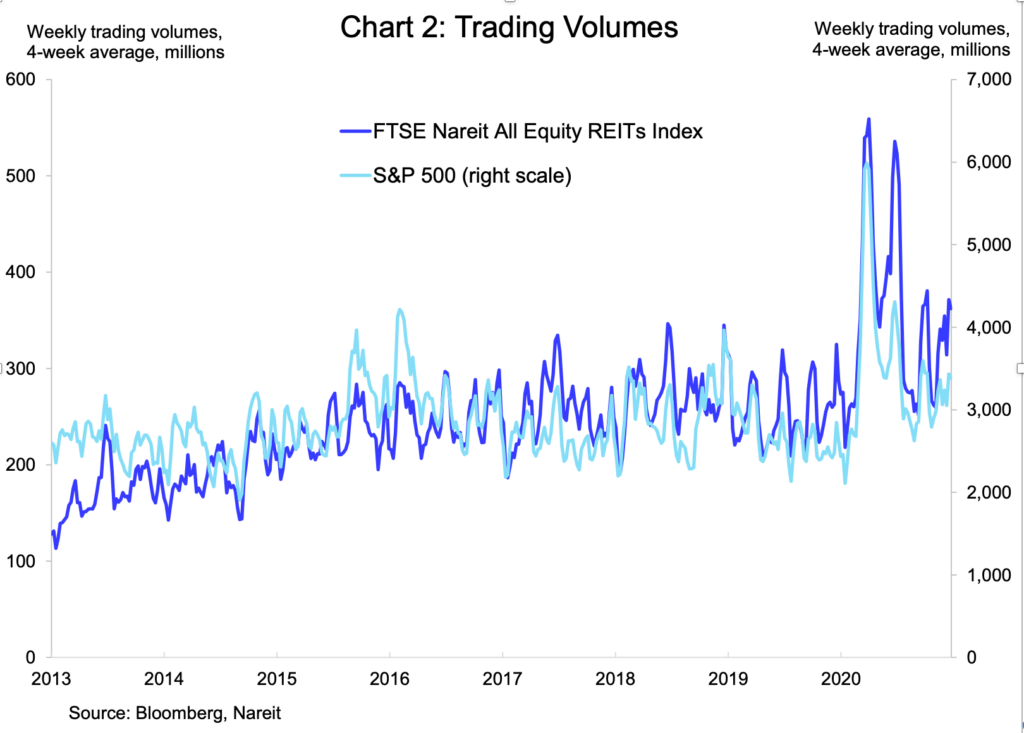

REIT share prices have risen steadily in early 2021, as evidence accumulates of the sector’s ongoing recovery. The FTSE Nareit All Equity REITs index posted total returns of 1% or more in five weeks in January and early February.

Outlook for 2021: The Pandemic and the Vaccines

The future of the pandemic and the success of the vaccines continue to hold the keys for the economy and commercial real estate—and for stock markets—in 2021. Early missteps in distribution of the vaccine, as well as further spikes in new cases and the troubling discovery of new, highly infectious strains of the coronavirus, have weighed on markets in the early days of the new year.

Most experts agree, however, that these challenges are mainly a question of timing—how quickly can a large enough share of the population be vaccinated to yield herd immunity? Whether progress accelerates and we begin to achieve herd immunity during the summertime, or new problems with vaccine distribution cause further delays, it appears highly likely that most parts of the U.S. economy will be mostly, or fully, reopened by the end of the year.

Future progress against the pandemic should allow people to return to stores and offices, and eventually to restaurants, movie theaters, and travel and hotels as well. The demand for all types of real estate will benefit from this recovery, boosting operating performance, earnings, and stock prices. At the same time, the economy will continue to undergo a digital transformation, creating challenges and opportunities across REIT sectors.

Economic policies are supportive of growth. Congress is currently debating the Biden Administration’s $1.9 trillion stimulus package, which is aimed at strengthening the fight against the pandemic and bolstering vulnerable parts of the U.S. economy, including workers who lost their jobs during the pandemic. In addition, the Federal Reserve has signaled it will continue its bond purchases to support financial markets and will keep interest rates low to help boost the recovery. These actions are likely to help ensure stronger overall economic growth and strengthen the fundamentals for all types of commercial real estate. REIT sectors that were hardest hit by the crisis, including lodging/resorts and retail REITs, should benefit as success against the pandemic allows a resumption of both business and holiday travel, and for shoppers to return to the malls, restaurants, and entertainment events.

REITs, especially those sectors with higher potential exposures to COVID-19, are likely to continue to rally in 2021, and perhaps outperform the broader market, as potential risks of a longer-term impact of the pandemic on real estate fade.

Calvin Schnure is Senior Vice President, Research & Economic Analysis, and joined Nareit in March 2011. He analyzes developments in the macro economy and their impact on REITs and commercial property markets, and on financial returns to REITs. He monitors performance of mortgage REITs and conditions in the U.S. mortgage market. He also conducts original research on REITs’ stock market returns and economic fundamentals. Mr. Schnure began his professional career in the 1990s as an economist at the Federal Reserve Board. While at the Fed he analyzed the non-bank financial sectors for the Flow of Funds Accounts, corporate profits, and commercial paper markets in the Capital Markets group, and also analyzed business fixed investment, including capital spending on nonresidential structures, for the Fed’s economic forecast. Subsequently he was Vice President for U.S. Economics at JPMorganChase, where he analyzed and forecast economic and financial market conditions, and advised senior management and clients. He was Senior Economist at the International Monetary Fund from 2002 through 2006, and Director of Economic Analysis at Freddie Mac from 2006 through 2011. Mr. Schnure earned a B.A. in Economics from Williams College, a Master of Arts in Law and Diplomacy from the Fletcher School at Tufts University, and a Ph.D. in Economics from the University of California, Berkeley.