The Energy Infrastructure Newsletter • Summer 2020

As an investment advisor, you have been subscribed to the Energy Infrastructure Newsletter so that you and your clients can stay abreast of this powerful emerging subsector. Formerly the MLP Newsletter, the Energy Infrastructure Newsletter is published in partnership with the Energy Infrastructure Council, a nonprofit trade association dedicated to advancing the interests of companies that develop and operate energy infrastructure. EIC addresses core public policy issues critical to investment in America’s energy infrastructure.

Westport, Conn.-based Energy Income Partners, LLC (EIP) manages $4.1 billion (as of April 30, 2020) in a long-only strategy targeting income and growth by investing in publicly traded equity securities of noncyclical energy infrastructure. EIP’s portfolio of pipeline and utility companies transport and/or deliver natural gas, electricity, and petroleum. EIP’s seven-member investment team collectively has more than 160 years of experience in the energy and utility industries.

![]()

Energy Sector Investments Focus on Stable Companies with Prospects for Growth

Advisor Access spoke with Jim Murchie, founder and CEO of EIP, about how investors can wisely position themselves in the energy infrastructure sector as the sector evolves and weathers times of uncertainty.

Advisor Access: The first half of 2020 has seen a lot of upheaval in the energy sector. Can you discuss the key issues that have driven share price volatility and weakness?

Jim Murchie: Simply put, the sector was hit with two black swan events. Dramatic price declines in crude oil due to the Saudis’ sudden decision to increase rather than cut production have been coupled with demand shock related to the coronavirus pandemic. These events triggered a massive, undifferentiated sell-off of energy pipeline and midstream companies, lowering valuations well beyond any expected reduction in earnings for many of these companies. The reason for this, in EIP’s view, was a massive deleveraging of the MLP-dedicated closed-end funds that held a significant portion of the shares of MLP-structured companies.

These recent events, in our view, significantly increase the likelihood of starkly lower capital spending by marginal players, and the conversion of the larger MLPs to C-Corps to access a wider, more liquid, and less volatile pool of capital.

Further, the upstream portion of the energy sector, which has long weighed on sentiment toward pipelines, has hit rock-bottom. Upstream now has no choice but to abandon its horrendous capital allocation and corporate governance practices, as it did after the oil price crash of 1986, an event that’s uncannily similar to what is unfolding this year. Saudi production increases, both then and now, aimed to “punish” noncompliance in the face of falling demand and rising non-OPEC

AA: Have this year’s events changed your investing strategy?

JM: No, just the opposite. Events like these prove the value of our strategy of owning companies with stable cash flows and higher dividend payout ratios, because that’s where we find the best returns. Doing that successfully means avoiding exposure to cyclical, commodity-driven merchant businesses, over-levered balance sheets, and weak management teams. We seek to manage the portfolios underlying our investment products as if an economic disaster will happen (because sooner or later one will), and that defensive posture has served us well in both up and down markets.

AA: Can you give some detail on your portfolio construction process?

JM: We look at the long-term financial history of each energy infrastructure company in North America. While share prices vary with market sentiment, we look for a steady, nonvolatile, rising progression in per share earnings and dividends over time, similar to the successful earnings track record found with consumer staples. That said, industries and companies evolve, and today’s energy transition means a successful strategy must continue to identify companies that can achieve stability and growth in the future.

At its core, the value of companies we seek to own centers on the incumbency of natural and legal monopolies, especially rights of way and franchise rights, to limited competition. We find these attributes in regulated utilities and long-lived, non-cyclical pipeline and storage assets with minimal commodity exposure. We look for demand-driven revenues from investment-grade customers. Above all, we emphasize owning companies with capable, proven management. Conversely, we seek to minimize uncontracted merchant businesses, commodity price exposure, short asset lives, excess leverage, supply-facing revenues, and exposure to weak counterparties.

AA: That sounds like it covers the downside, but how do you achieve growth?

JM: That’s because, apart from maintaining portfolio diversification, we are agnostic to whether a company is formed as a C-Corp, an MLP, or—back in the day—a Canadian income trust. Our approach is also indifferent to a company’s inclusion in an index, because we are active managers. As long as the attributes mentioned above are present (while maintaining portfolio diversification), we’re equally attracted to the following business activities:

- Pipelines, storage, and terminals;

- Transmission and distribution of electricity and natural gas;

- Low-cost renewable energy developers selling on long-term contracts.

- That’s provided, of course, companies can generate earnings and dividend growth, and stability, over the long term.

AA: You’re describing a highly active management strategy, yet only about 5% of active managers actually outperform the market or the relevant index.

JM: That’s generally true of broader market indices, but over our 17-year history, we have succeeded in outperforming most indexes, especially the narrower ones like the Alerian MLP Index. Narrower indexes tend to be based on quantitative screens or themes. For example, in energy, that has meant being structured as an MLP or having exposure to a theme like “shale drilling.”

We believe the advantages of an active strategy include being able to evaluate the quality of a management team, determine whether a business is supply- or demand-facing, and incorporate other factors, such as cost efficiency, environmental impact, and relationships with regulators and policy makers. In our view, most indexes don’t take these things into account. But the factors listed above have a material impact on earnings stability, earnings growth, and ultimately an investor’s total return.

AA: You mentioned the “energy transition.” Don’t you worry about investing in a buggy-whip strategy, as customers increasingly go off the grid and make their own energy with solar panels and batteries?

JM: No. In fact, our strategy focuses on companies that benefit from ongoing evolution of the energy system. For the last 200 years, four attributes have driven change in how a society uses primary sources of energy to power its economy: cost, reliability, safety, and environmental impact. Think of modern society’s transition from burning wood to mining coal, which gave way to the growth of petroleum and then natural gas, all driven by the desire for lower costs and a cleaner environment. Think of how safety and environmental impact today drive public willingness to embrace renewables over traditional resources. And finally, reliability is not just about the inconvenience of power going out for an hour—which is far more costly for today’s Internet-driven economy—it’s also a national security issue.

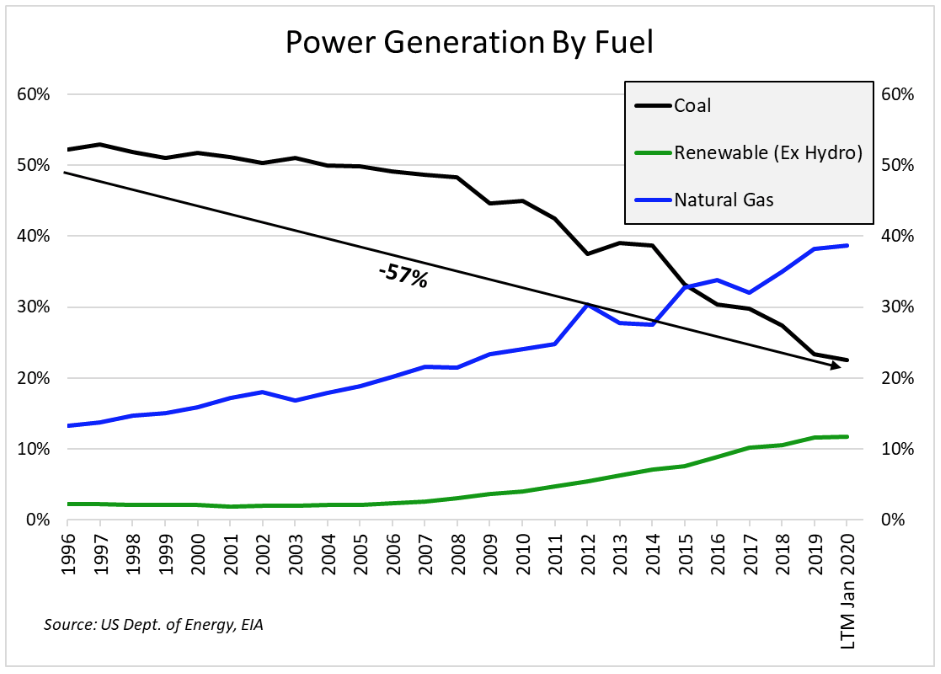

For the successful utilities, this has meant an accelerating transition away from costly, inefficient, and environmentally harmful coal-fired generation. As illustrated in the chart below, power is increasingly being sourced from natural gas, as well as from increasingly cost-competitive wind and solar made possible through the backup flexibility of natural gas-fired electric power.

The incorporation of modern technology, coupled with “smart grid” automation, data analytics, and artificial intelligence, is driving lower cost and greater reliability to consumers while mitigating environmental impact. Those investments are also driving mid- to high-single-digit earnings growth in an industry that hasn’t seen growth for decades. That trifecta of consumer benefit, public policy alignment, and earnings returns is hard to find.

Source: Energy Information Administration (as of January 2020).

For the vast majority of customers, “cutting the cord” would reduce reliability and significantly drive up cost, as their investment in solar panels and batteries would have to be large enough to provide power for infrequent peaks or long stretches of cloudy weather, causing the resources and investment to go underutilized most of the time. Staying connected to an increasingly intelligent network, run by the legacy, investor-owned utilities, in our opinion, optimizes the use of shared resources, lowers costs, and increases reliability, similar to the Internet and cloud computing. Over investing in battery storage capacity at each location would simply be repeating the inefficiencies of the older system we are trying to replace.

Today, 13 U.S. states, districts, and territories, and over 200 localities, have implemented some form of requirement to transition to 100% clean energy and/or carbon neutrality over the coming 20 to 30 years.* The network utilities and incumbent gas pipeline network that facilitate continued growth of wind and solar form the backbone of a partnership that is delivering cheaper, cleaner, safer, and more reliable energy.

AA: Thank you, Jim.

* Source: University of California Los Angeles Luskin Center for Innovation, “Progress Toward 100% Clean Energy,” November 2019

James Murchie is the President, Founder and CEO of Energy Income Partners and Portfolio Manager of EIP’s Funds. He founded EIP in 2003 and is the portfolio manager for all of its funds which are concentrated on high-payout energy infrastructure securities within asset classes such as Master Limited Partnerships (MLPs), MLP affiliates, Utilities and Yield Corporations (YieldCos) and Energy Infrastructure Real Estate Investment Trusts (REITs). Jim holds degrees from Rice University and Harvard University.