Skip to content

Search for:

Home

Featured Companies

Healthpeak Properties

NNN REIT

LTC Properties

COPT Defense

Enterprise Products Partners

Southern Company 2024

Essential Utilities

Federal Realty

Williams

1.800.FLOWERS.COM

CVS Health

CMS Energy

Southwest Gas Holdings

EIC Newsletter

Summer 2025

Spring 2025

Winter 2024

Fall 2024

Summer 2024

Spring 2024

Winter 2023

Fall 2023

Summer 2023

Spring 2023

Winter 2022

Fall 2022

Summer 2022

Spring 2022

Winter 2021

Fall 2021

Summer 2021

Spring 2021

Winter 2020

Fall 2020

Summer 2020

Spring 2020

Winter 2019

Fall 2019

Summer 2019

Spring 2019

Winter 2018

Fall 2018

Summer 2018

Spring 2018

Winter 2017

Fall 2017

Summer 2017

Spring 2017

Winter 2016

Fall 2016

Summer 2016

Spring 2016

Winter 2015

REIT Newsletter

Summer 2025

Spring 2025

Winter 2024

Fall 2024

Summer 2024

Spring 2024

Winter 2023

Fall 2023

Summer 2023

Spring 2023

Winter 2022

Fall 2022

Summer 2022

Spring 2022

Winter 2021

Fall 2021

Summer 2021

Spring 2021

Winter 2020

Fall 2020

Summer 2020

Winter/Spring 2020

Fall 2019

Summer 2019

Spring 2019

Winter 2019

Fall 2018

Summer 2018

Spring 2018

Winter 2018

Fall 2017

Summer 2017

Spring 2017

Winter 2017

Fall 2016

Spring 2016

Fact Sheets

COPT Defense Properties

Williams

Archrock

Kimco Realty

NNN REIT

Federal Realty

1-800-FLOWERS.COM

Magellan Midstream Partners

ONEOK

W. P. Carey

Enterprise Products Partners

Media Kit

Contact

Subscribe

Corporate Office Properties Trust Fact Sheet

advisor001

2025-05-29T21:15:30-07:00

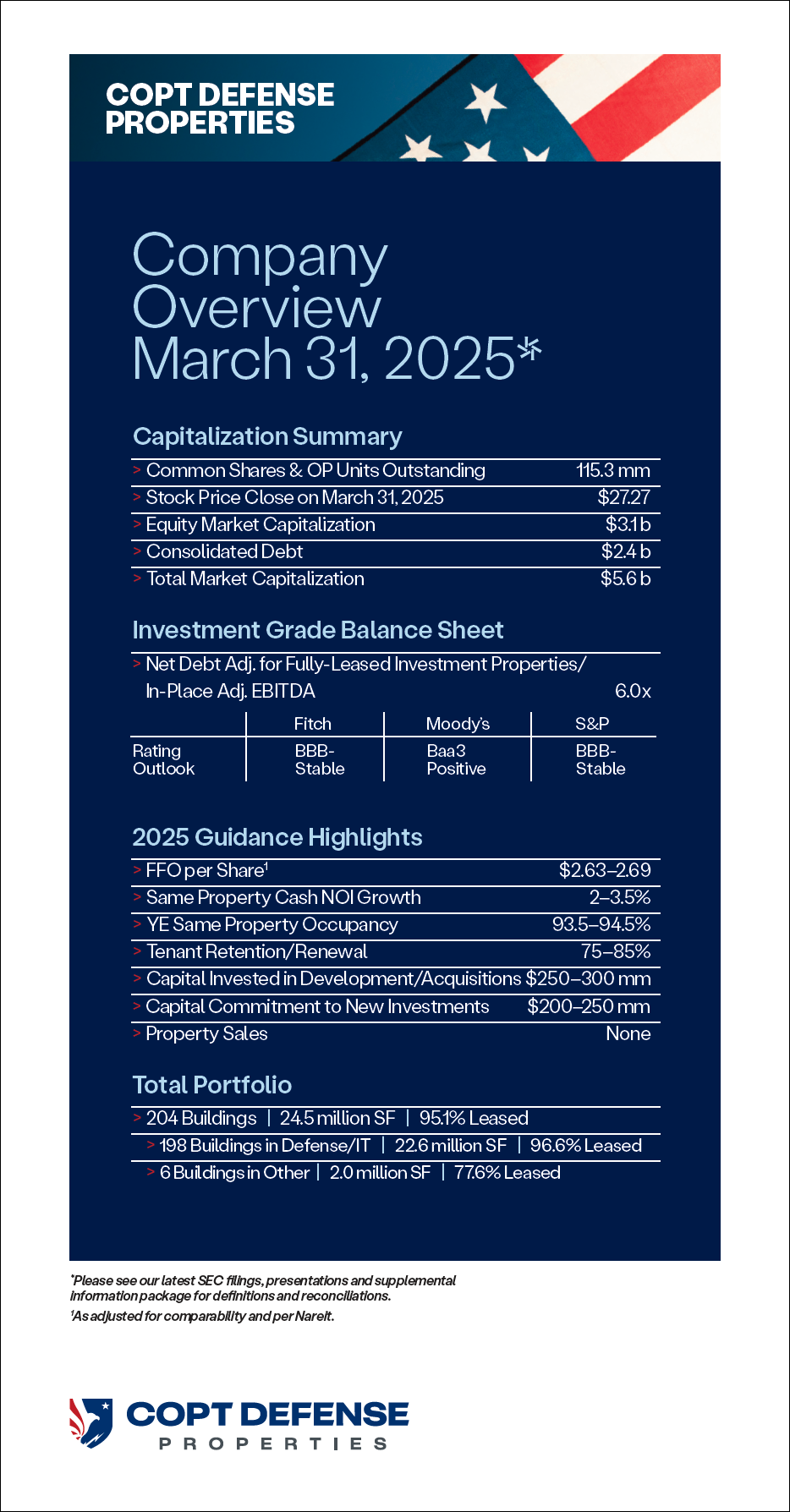

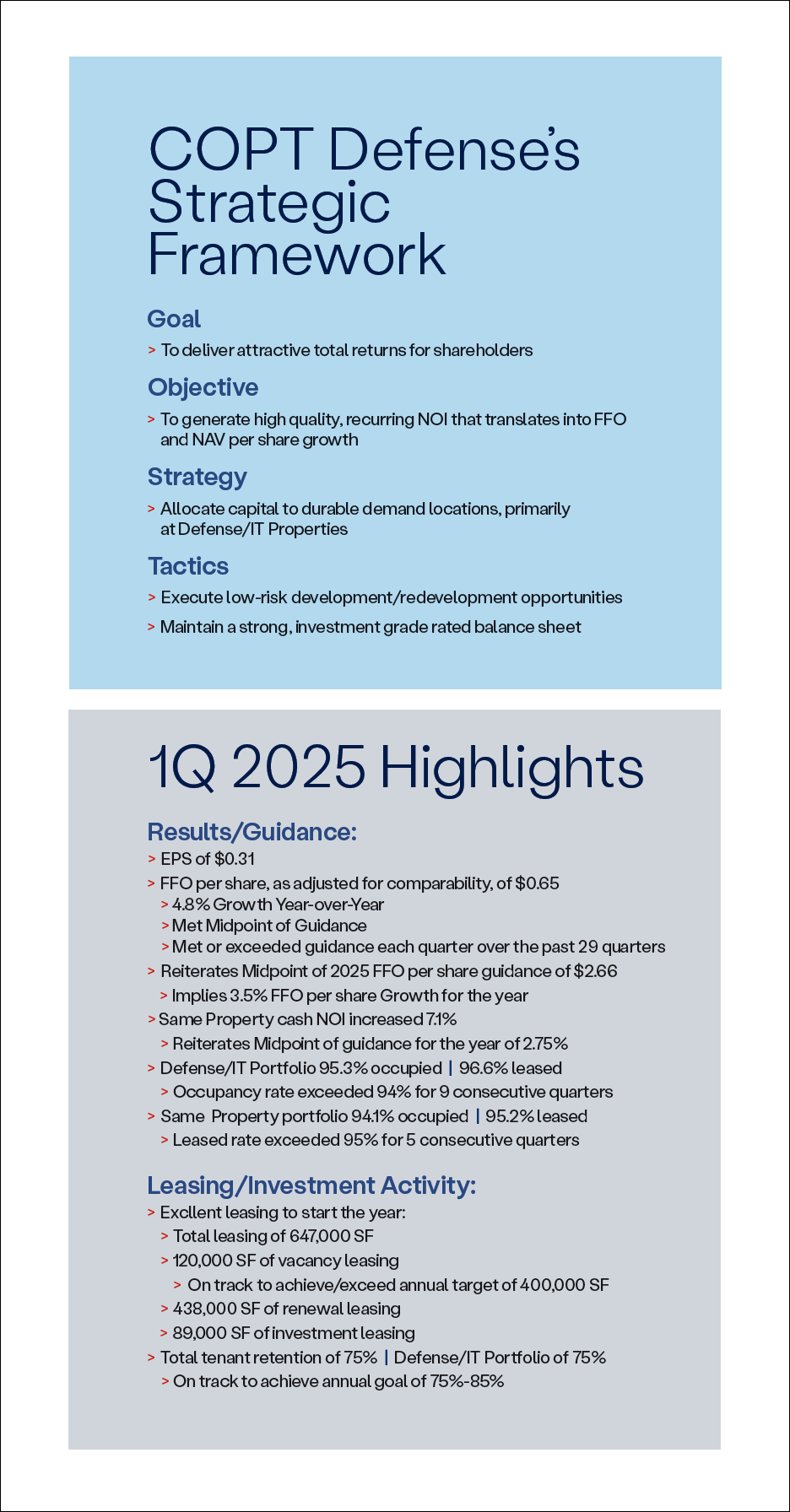

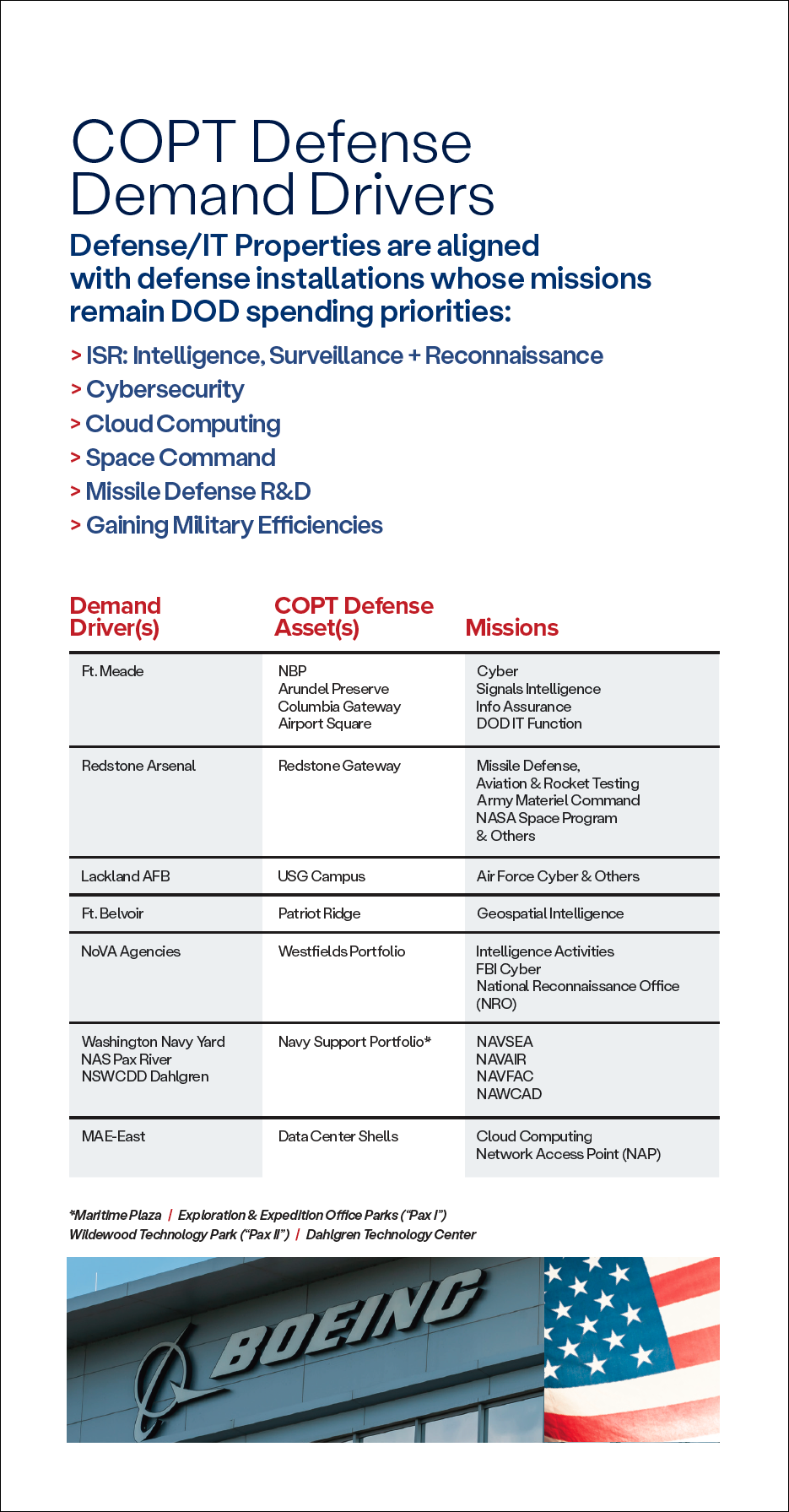

Click here to download the COPT Fact Sheet in PDF format.

CLICK HERE TO DOWNLOAD THE COPT DEFENSE PROPERTIES FACT SHEET

Go to Top